Paragon Advanced Labs Has Multibagger Potential

Initiating Long Position in the MCO Portfolio

Paragon Advanced Labs (PALS.V) (PAVLF) Cap Table

Shares Outstanding: 32,402,262

Options & Warrants: 1,174,310

Fully Diluted: 33,576,572

I came across Paragon Advanced Labs while researching companies for the upcoming 2026 Planet MicroCap Conference. My plan was to put the best candidates on a watchlist, gather more information at the conference, and then decide on inclusion. Paragon meets the major MCO criteria for inclusion as a Multibagger: a moat, a large TAM with limited competition, a credible capture plan, and a clear path to profitability, as described here. I look forward to the conference, but I see no reason to delay adding the position to the MicroCap Opportunity (MCO) portfolio.

A key element in my investment process is speaking with management, which I have not done yet. Ian Cassel and Jeff Kowal provide a first-class fireside chat with Paragon’s CEO, Peter Shippen, in a MicroCapClub Business Breakdown video, which sealed the deal for me.

I’ll be doing due diligence on each of the companies I plan to speak with at the conference and will feature these deep dives in separate articles for each stock. These write-ups will only be available to premium subscribers. An updated article without a paywall will be added should any of these stocks be added to the MCO portfolio.

The Investment Thesis

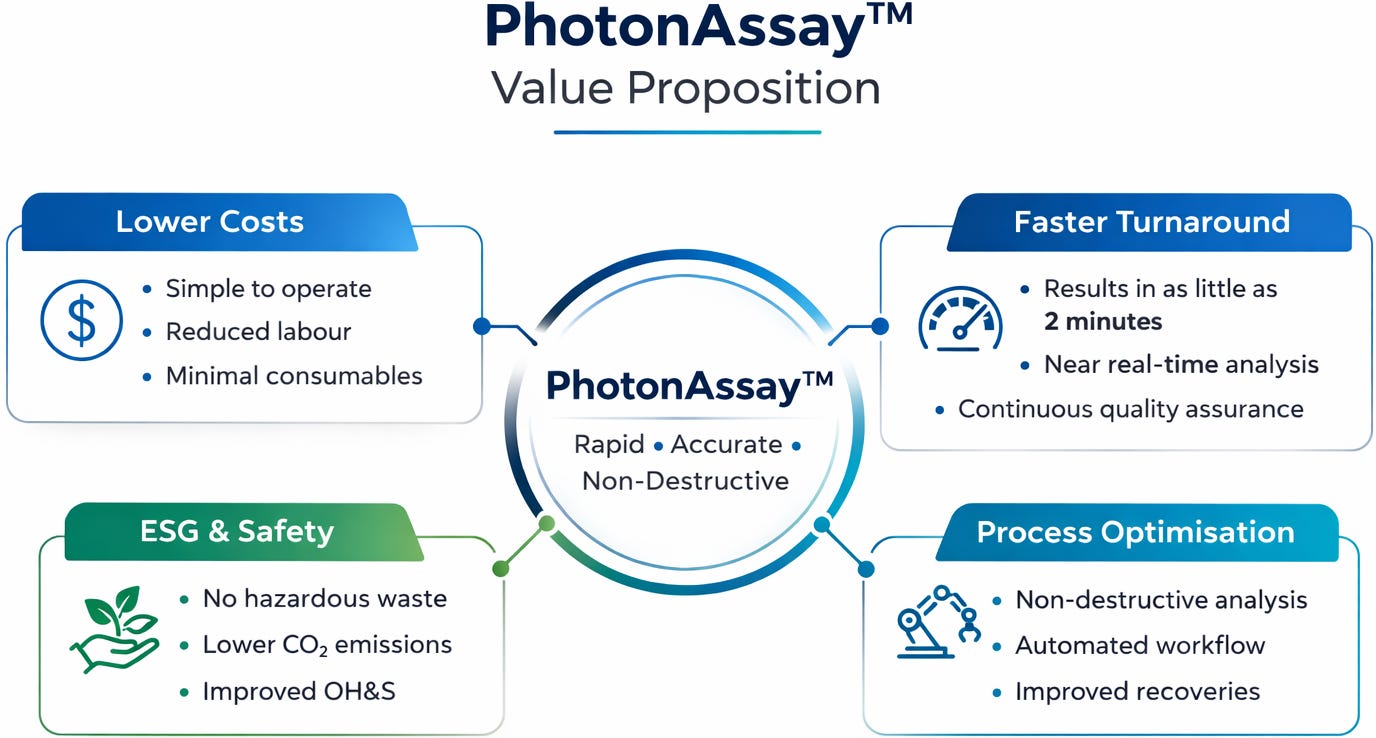

Paragon is a microcap operator of PhotonAssay (PA), the only commercial technology in decades to meaningfully threaten fire assay, the industry standard for analyzing precious metals for the past century. PA is faster, more accurate, safer, and environmentally cleaner. PA is in the early stages of replacing fire assay. Paragon and its technology partner Chrysos (CHRCF) are, to my knowledge, the only pure public plays on PhotonAssay.

In this write-up, I cover the demand for PA, the benefits of PA over fire assay, and how the Paragon-Chrysos partnership works, Paragon’s moat, the competitive landscape, the business plan, the path to profitability, the risks, and why Paragon offers more upside than Chrysos, and what I want to learn about Paragon at the conference.

Demand Is Outpacing Supply

The underlying demand for PA capacity comes from three forces:

Drilling activity is at multi-year highs. Higher gold and copper prices have made marginal deposits viable, increasing exploration drilling. The capacity in the legacy system simply cannot absorb the increased volume.

Waiting increases cost. Slow assay returns mean ore is being mined and stockpiled before grade is confirmed, leading to dilution and recovery losses.

More demand than supply. Chrysos is the only significant PA system manufacturer in the world, and its manufacturing capability is not keeping up with demand. Paragon has built this equation into its moat.

The willingness to pay for speed shows up in the pricing structure. Mining companies routinely pay rush-order premiums for priority assay processing. Paragon’s standard pricing is the same as what fire assay labs charge for premium rush rates. PA is underpriced relative to the value it delivers due to the quick turnaround. Paragon can offer a 20% discount on fire assay pricing during the adoption phase and still achieve attractive unit economics.

The geography of the pull also matters. Canada is the most competitively priced assay market globally due to its high lab density. The price in the underserved regions are 50% higher per sample than in Canada. This is the rationale for Paragon’s geographic strategy: place machines in underserved regional markets where the pricing premium amplifies the unit economics.

PhotonAssay vs Fire Assay

Mining companies need to know what’s in the rock they pull out of the ground.

Fire assay has been the standard methodology since the late 1800s. Fire assay works by mixing a small sample of crushed rock with a chemical solution that dissolves the precious metals from the rock. The mixture is melted in a high-heat furnace, eventually dissolved in acid, and analyzed.

Under normal market conditions, the fire assay turnaround takes 3–10 days end-to-end. In the current cycle, with global drilling activity surging, it’s running 3–12 weeks. Mining companies need live data to make decisions. This is the problem that PhotonAssay addresses.

PhotonAssay uses a much larger sample than fire assay and places it in a sealed plastic container. The container moves through a machine the size of a tractor-trailer that bombards it with high-energy X-rays. The X-rays excite atomic nuclei in the sample, which emit characteristic gamma signatures that identify and quantify the elements present.

The advantages of PhotonAssay are;

Speed. 2–3 minutes per sample

Sample size and accuracy. Fire assay tests 10–50 grams. PA tests 250–650 grams. Gold is unevenly distributed in coarse particles within a rock, making the small fire assay sample statistically inadequate.

Non-destructive testing. Fire assay destroys the sample. PA preserves it. This means PALS can offer Geochem analysis (multi-element scanning) on the same sample that just went through PA, generating an additional revenue stream that fire assay operators cannot. Roughly 80% of gold and silver samples get a Geochem add-on at Paragon facilities.

Safety and environmental profile. Fire assay involves toxic chemicals (lead oxide, fluxes, acids), high-temperature furnaces, and hazardous waste streams. PA uses no chemicals, no smelting, and no toxic byproducts.

Multi-element capability. PA currently detects gold, silver, and copper. A software upgrade in development will add 11 additional elements (zinc, lead, uranium, and others), without requiring hardware changes. Fire assay typically tests for one element at a time.

Data quality and digital integration. PA results are delivered as digital files directly to clients. Fire assay still relies heavily on manual data entry and paper trails.

How the Chrysos Partnership Actually Works

Paragon licenses the technology from Chrysos, whose business model is pure technology-as-a-service. They do not operate any commercial assay labs. They do not perform first-hand testing. They lease PA units to mining companies and laboratory companies and earn revenue through a combination of fixed leasing fees and variable per-sample fees. Their gross margins consistently run above 60%, reflecting the pure-IP nature of the business.

Chrysos’ lease agreements are typically 5 to 15 years, with 18–24 months of territorial exclusivity per machine. Chrysos is also not dependent on any single operator. It serves a wide range of customers internationally. Paragon is not a unique or favored partner, but is one of several. That symmetry stabilizes the relationship.

The economic structure aligns both sides. Chrysos collects a six-figure deposit on each machine plus a per-assay royalty of approximately C$7–8. Once a machine is placed, Chrysos’s incentive is for it to run hot, as every assay is a royalty. Paragon has the same incentive. Both sides win when machines are well-utilized. Both sides lose if a region becomes oversaturated and prices collapse.

The TAM and Competitive Map

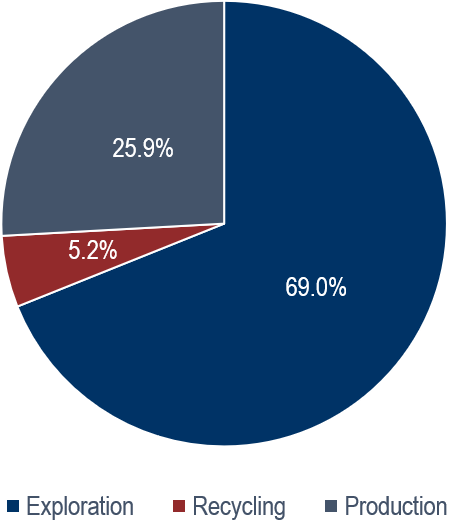

The fire assay TAM is worth C$5.3B globally, with over two-thirds exploration and one-quarter production.

The top four incumbent labs (ALS, SGS, Bureau Veritas, Intertek) collectively hold 25% of the fire assay market share. The remaining 75% is fragmented across hundreds of regional and mom-and-pop labs.

The top four incumbent labs are direct beneficiaries of scarcity in fire assay capacity, but they are also the most motivated to access PA capacity to defend their customer relationships.

The Scale of the Replacement Cycle

Chrysos reports that the top 20 global gold producers have already engaged with PA technology and that sample volumes were running 950,000 per month in early 2026, up 53% year-over-year.

Goldman Sachs noted in its research coverage of Chrysos that, as of late 2025, Chrysos had deployed roughly 40 units, yet it still serves less than 5% of its global addressable market for gold mining. Displacing the existing fire assay base for gold alone would require approximately 600 PA machines in operation. It is estimated that about 800 PA systems will be needed to fully replace the use of fire assay. As of May 2026, Chrysos has accelerated its deployment of PhotonAssay units, with 44 units currently deployed and 72 contracted. Chrysos production capacity is estimated at 20 units annually. At Chrysos’s current production rate, that is a 30-year buildout just to replace the fire assay’s gold workload. Chrysos is actively scaling up production and plans to accelerate deployment in 2027. Deployment is expected to reach 78 units by year-end 2028.

Chrysos is planning on adding software for 11 additional elements. The required PA fleet to displace fire assay across all the elements PA is on track to detect runs into the thousands of machines. Even if Chrysos doubles or triples its annual production capacity, it will still be on a multi-decade adoption curve.

Paragon’s business plan, discussed below, features scarcity as part of its competitive moat. The big-four incumbent labs collectively own only ~25% of the contracted PA fleet through 2027, leaving Paragon with the world’s largest commercially open PA fleet.

PA planned capacity allocation for the first half of 2027:

MSA Labs: 35% (largely tied to specific large customers like Barrick/Newmont)

Paragon: 20%

SGS: 10%

ALS: 8%

Intertek: 7%

Other operators and direct mine-site placements: 20%

The Moat

The moat sits in the contract architecture and the capacity bottleneck behind it:

Contractual exclusivity. Each placed unit carries 18–24 months of regional exclusivity within a 100–200-mile radius, embedded in a 5–15-year overall lease. Paragon’s first machines (Hamilton placed mid-2023; Surrey, August 2024) are already at or past initial exclusivity. Newer placements (Sparks June 2025, Mexico Q2/26, plus 8 more by H1/27) carry exclusivity windows running through 2027–2028 and beyond.

Capacity scarcity. Chrysos manufactures 20 units per year. Total industry deployment will be 78 units by YE 2028 against a fire assay TAM that would require 600+ units to displace. A new entrant cannot get capacity. Even existing operators cannot rapidly scale beyond their current contracted slots. Paragon controls 20% of the global pipeline.

Operational lock-in once a customer switches. Mining companies that adopt PA as their standard are unlikely to revert to fire assay. The deployed Chrysos fleet running at 82% utilization is the proof point: once placed, machines stay busy.

Geographic density via hub-and-spoke. Paragon has built sample preparation facilities in Timmins (ON), Thunder Bay (ON), and Coeur d’Alene (ID, via the Scout Discoveries partnership, that feed the Hamilton and Surrey hubs. Combined Timmins and Thunder Bay capacity already covers Hamilton’s full PA throughput.

McEwen as strategic anchor. Rob McEwen owns 27% of Paragon via a C$15.3M cash investment at C$1.75 with no warrants. He is also the CEO/founder of McEwen Mining (MUX), a Paragon customer. He’s a customer, an investor, and a source of industry credibility. His relationships in gold mining open doors that a microcap company would not otherwise reach.

The Plan

Laurentiu Fulea was hired in April as Canadian Operations Manager. He came from ALS, where he ran West Africa operations across seven countries. His arrival opens a credible international expansion pathway that Paragon previously lacked the in-house experience to execute. The plan to capture market share is concrete, contracted, and partially executed:

3 machines operational today — Hamilton ON (running since May 2023), Surrey BC (August 2024), Sparks NV (June 2025)

6 additional machines this year.

3 more machines in H1/27 and an additional 3 more machines before the end of 2027.

Hub-and-spoke build-out- sample prep facilities in Timmins, Thunder Bay, Coeur d’Alene are already operational. Sparks Geochem capacity doubling near completion.

Regional monopoly strategy — focus on underserved markets where pricing runs 50% above competitive Canadian rates

Strategic partnership model — Scout Discoveries (vertical integration with a US explorer with five core drill rigs); consortium deals with mid-tier producer groups; potential capacity-sharing arrangements with the big-four labs that need PA units but face Chrysos’s manufacturing queue.

The Path to Profitability

The path to profitability is already baked in. Paragon generated C$4.4M of revenue across the nine-month transitional fiscal year that ended December 31, 2025. The seasonally strongest quarter of that period (October through December) produced C$1.8M, roughly in line with broker estimates. Forward guidance is what should be attracting investors’ attention. Q1 is historically the weakest quarter for northern markets. Management guided to revenue of C$2.2M, a 21% sequential gain that delivers nearly half of all of FY2025’s nine-month revenue in a single quarter. April 2026 alone came in 40% above any prior month in the company’s history, and management has indicated that the rest of 2026 is tracking ahead of April.

The driver behind the step-change is a single customer contract worth more than C$8M annualized that began ramping in late February. Q1 captured roughly one-third of its steady-state contribution; the remaining two-thirds rolls in progressively through Q2. EBITDA breakeven is at approximately C$1.5M in monthly revenue, which the current trajectory is expected to cross in late Q2 or Q3 of 2026. The near-completion of the Sparks Geochem capacity doubling (~C$500k capex, ~3-month payback per management) layers high-margin attach revenue onto existing samples and pulls breakeven closer.

The Financial Bridge to Profitability

Each PA unit carries roughly C$32,500 of fixed monthly lab overhead (rent, base staffing, Chrysos engineers). The variable costs are C$8 royalty to Chrysos and C$0.50 per sample jar.

Revenue per machine:

30% Utilization = C$3.4M annual revenue and C$1.8M annual EBITDA

60% Utilization = C$6.8M | C$4.0M annual EBITDA

80% Utilization (full operational target) = ~C$9.0M |~C$5.5M annual EBITDA

A machine moving from 30% to 80% utilization roughly triples its EBITDA contribution. Twelve machines at 80% utilization produce approximately C$110M in revenue and C$66M in EBITDA before corporate overhead. Subtract C$6–8M of corporate G&A and C$5–6M of depreciation to reach consolidated EBIT.

The capital plan supports the buildout without dilution. The RTO raised ~C$16M in December 2025; net debt today is C$5.9M. Each incremental machine requires roughly C$600k in buildout capex (sometimes partially absorbed by partners — the Scout Discoveries deal is structured this way), plus a six-figure deposit to Chrysos. Management has indicated that RTO cash combined with 2026 operating cash flow of approximately C$7.5M is sufficient to fund all nine incremental machine deployments through H1/27 without a dilutive raise.

Gross Margin Expansion

Gross margin scales hard with utilization because lab overhead is fixed. The Chrysos royalty (C$8 per sample) and per-jar consumables (C$0.50) are variable; lab rent, base staffing, and Chrysos engineers are fixed at roughly C$32,500 per machine per month.

The 60–65% mature gross margin lines up with what Chrysos itself reports at the technology layer. At maturity, both businesses are essentially earning technology rents, and PALS captures an additional layer (Geochem attach, sample prep, regional pricing premiums) that Chrysos does not.

The ramp from 30% to 60%+ gross margin between 2026 and 2028 is the operational leverage that drives the share price. Revenue roughly triples in that window. EBITDA goes up roughly 5–7x.

Why Paragon Has More Upside Over Chrysos

Both Paragon and Chrysos are plays on the displacement of fire assay by PhotonAssay over the coming decade. The multiple gaps tell most of the story of which stock has the higher potential return. Chrysos trades at 19.4x 2026E and 13.8x 2027E EV/EBITDA. Paragon trades at 12.2x 2026E and 5.8x 2027E. That’s a 2.4x multiple gap on 2027 numbers. The market is paying up for the IP/recurring royalty model and discounting the operator for execution risk. The discount is too steep, given how much of the execution is already contracted.

Six reasons why Paragon offers a better risk-adjusted return:

Better operational leverage: Chrysos has corporate-level leverage with a fixed per-assay royalty, while Paragon has both the corporate layer and the per-machine layer above fixed costs.

Geographic monopoly pricing. Chrysos collects the same royalty regardless of where the machine sits.

Add-on revenue streams. Paragon captures meaningfully more revenue per sample than the PA royalty implies. Chrysos earns nothing on any of that.

McEwen chose the operator, not the IP.

Capacity-constrained supply. Paragon benefits from the PA system demand more than Chrysos. Chrysos’s royalty rate is contractually fixed regardless of where end-customer pricing goes. Chrysos can’t make more machines faster without major capex, and even if they did, oversaturation would crush their own royalty economics.

The simple way to frame it is this: Chrysos is a high-quality compounder priced accordingly. Paragon is an operationally leveraged, capacity-constrained regional monopoly priced at a 60% discount to that compounder on 2027 EBITDA.

Price Targets and Valuation

12-month target: C$8.00 (+150%)

13x multiple applied to 2027E EBITDA of approximately C$22M — slightly ahead of Clarus’s C$19M because the trajectory through April suggests existing machines will hit 40–50% utilization by year-end 2026. The 13x multiple is a premium to legacy lab comps (avg ~11.4x) reflecting growth, and a discount to Chrysos at 13.8x 2027E reflecting operator vs. IP risk. Implied EV: ~C$265M.

24-month target: C$12.00 (+275%)

Same 13x multiple on EBITDA of ~C$30M, assuming 50% blended utilization across a 10–12 machine fleet by the end of 2027, with the 20% pricing discount partially phased out. Implied EV: ~C$395M.

3-year target: C$22–30

Full utilization at 80%, discount eliminated, regional pricing premiums emerging in underserved markets. The Multibagger scenario.

Comp multiples (2026E EV/EBITDA): ALS 13.7x, Bureau Veritas 10.0x, SGS 11.4x, Intertek 10.6x, Chrysos 19.4x. PALS at 12.2x 2026E and 5.8x 2027E. The 2027E multiple is the one that matters, and it’s a discount to slower-growing incumbents and a steep discount to the technology owner.

Risks

I based my investment assumptions on execution of the 9 incremental machine deployments. Timing slippage, commissioning delays, and ramp delays are risks that cannot be foreseen or predicted. The Mexico unit (the 4th machine) has already had a slight delay into Q2/26. Other risks to consider are :

Utilization ramp speed. Newly deployed machines will have an onboarding period.

Chrysos relationship. Fully addressed below.

Commodity cycle exposure. Drilling activity tracks commodity prices. A meaningful gold/copper drawdown softens the assay TAM.

Post-exclusivity defensibility. The 18–24 month per-unit exclusivity will start rolling off in early markets. Switching costs and Chrysos’s incentive to protect royalties help, but neither is airtight.

Customer concentration. A single C$8M+ contract represents 25% of 2026E revenue.

Pink Sheet listing - The stock is listed as a fully reporting entity in Canada but not in the U.S. This is not atypical for an early commercial-stage company that is saving expenses by avoiding higher filing and listing fees.

The Chrysos relationship is the most important risk to consider. Termination risk and margin-squeeze risk could undermine the investment thesis. The starting point is not a concern because the two entities’ business models require a working partnership. I break down the partnership risks as:

Termination of the partnership. The likelihood that either partner will terminate the partnership before the contract end date is low because of the symbiotic relationship.

Chrysos bankruptcy or capital problems. Their financials are strong. H1/26 EBITDA was up 152% on revenue up 50%. Gross margins above 60%. Growing revenue base of long-dated lease agreements. Not a near-term concern.

Technology obsolescence. PA is the only commercial breakthrough in fire assay alternatives in decades.

Acquisition of Chrysos by a third party. This is unknown territory because the actual contract terms are not publicly disclosed.

My Vegas Questions

What are the change-of-control provisions in the PALS-Chrysos master agreement?

Blended utilization across the three active machines as of the end of Q2/26 and the trajectory month-over-month from February forward.

The C$8M+ contract. Single customer? Multi-mine? Renewal terms?

Mexico machine status and pricing.

McEwen’s role beyond passive shareholder. How is the MUX customer relationship structured commercially? Strategy involvement, customer introductions to other miners, board guidance?

Chrysos parts diversification. Status on alternative sourcing for China-supplied components.

International expansion. With Fulea on board and his West Africa background, what’s the next geographic target after Mexico?

M&A interest in Paragon. At what fleet size does Paragon become acquisition-relevant?

Post-exclusivity defensibility. Playbook to hold regional share once Chrysos exclusivity rolls off in early markets.

11-element software upgrade. Timing, expected revenue uplift per machine, and customer demand signals.

Geochem economics. Actual attach rate at Hamilton and Surrey, per-machine Geochem revenue ceiling at full utilization.

Capital plan. Sufficiency of RTO cash + operating cash flow to fund the 12-machine target. When does free cash flow turn?

OTC uplisting. Timing and expected impact on US institutional engagement.

Conclusion

Paragon meets all the criteria for inclusion in the MCO portfolio: a real moat, a large TAM with limited competition due to a manufacturing capacity bottleneck at the technology owner, a credible plan to capture the largely already contracted opportunity, and a clear path to profitability.

If they execute, this is a multi-bagger.

Disclaimer: The MCO portfolio consists of microcap stocks we invest in. Our write-ups are our research efforts and are not financial advice. We have absolutely zero consideration for your financial circumstances or risk factors, as we are not financial advisors. Do your own due diligence.

It looks interesting ..

Sergio has a good record of finding interesting companies ..

I may open a position this week ..